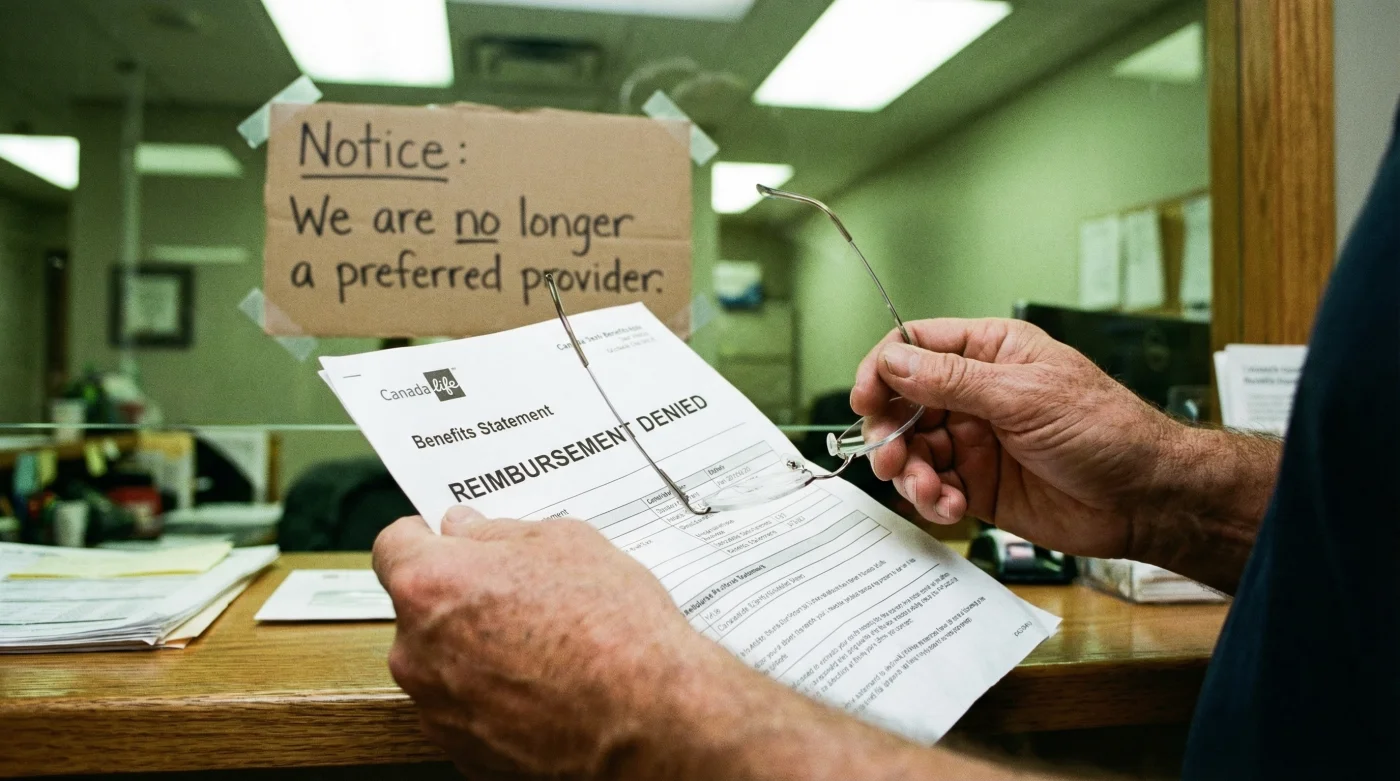

Millions of Canadians trust their employer-sponsored health benefits to cover routine medical expenses, assuming their preferred local practitioners are automatically eligible. However, a quiet but monumental shift is currently catching thousands of policyholders off guard, leaving them with unexpected, out-of-pocket bills right at the clinic counter. As seasonal vision checks peak across the country, many are discovering that their traditional freedom to choose any independent eye care professional has been abruptly revoked without adequate warning.

This massive change in how Canada Life processes optical reimbursements marks the end of an era for standard healthcare flexibility in Canada. By permanently restricting vision claims strictly to an approved network, the insurance giant is forcing a massive migration of patients away from independent optometrists. Yet, buried within the updated policy documents lies one crucial administrative loophole—a specific sequence of steps that savvy claimants are using to safeguard their coverage before their next eye exam.

Understanding the Exclusive Provider Network Architecture

For decades, Canadian employees enjoyed a decentralized approach to vision care, confidently visiting neighbourhood clinics from Victoria to Halifax. The new Canada Life mandate dismantles this open-market system, implementing a strict Preferred Provider Organization (PPO) model. This means that if an optometrist or optician is not formally registered and active within their specific corporate network, your receipt becomes practically worthless for reimbursement purposes. Actuarial studies confirm that closed-network models save insurers up to 22 percent annually, but these savings often translate into a severe restriction of choice for the end-user. The impact is especially devastating for residents living 50 kilometres or more from major metropolitan centres, where corporate in-network clinics are sparse.

| Coverage Aspect | In-Network Providers | Out-of-Network (Independent) Providers |

|---|---|---|

| Reimbursement Rate | Up to 100% of eligible policy limits | 0% (Strictly out-of-pocket) |

| Direct Billing | Fully automated at the point of sale | Manual submission strictly denied |

| Audit Risk | Virtually eliminated | Extremely high, leading to automated rejection |

| Product Selection | Limited to corporate partner catalogues | Unrestricted, but entirely un-funded |

Healthcare consultants emphasize that this shift is not a temporary administrative glitch, but a permanent structural realignment designed to control escalating material costs across the benefits sector. To truly grasp the financial stakes, we must examine the exact diagnostic triggers that lead to an immediate claim rejection.

Diagnosing Claim Denials and Financial Mechanics

With the implementation of these stringent network rules, the automated adjudication algorithms have become completely unforgiving. Patients who attempt to submit claims the traditional way are encountering instant digital roadblocks. Experts advise that understanding the specific rejection codes is paramount to avoiding severe financial penalties when purchasing prescription eyewear or booking specialized diagnostic tests like corneal topography.

- Symptom = Claim instantly rejected with ‘Code 44’: Cause = The servicing clinic has not completed the mandatory network onboarding, classifying them as an out-of-network entity.

- Symptom = Partial reimbursement on premium lenses: Cause = The provider is in-network, but the specific polycarbonate or anti-reflective coating exceeds the newly adjusted maximum allowable limits.

- Symptom = Direct billing portal locked: Cause = The patient’s file has not been synced with the updated Lumino Health or equivalent network directory mapping.

To navigate this landscape, policyholders must adhere strictly to the new ‘dosing’ requirements of the policy. You must submit your claims within exactly 30 days of the service date, ensuring the optical invoice reflects a zero-dollar outstanding balance if coordinated with a secondary provincial payer. Furthermore, you must verify that the provider’s 10-digit Provincial Registration Number is flagged as active in the member portal at the exact time of the transaction.

| Technical Mechanism | Policy Metric (The ‘Dose’) | Critical Enforcement Action |

|---|---|---|

| Network Verification Window | Minimum 48 hours prior to appointment | Failure to pre-verify guarantees a 100% claim denial. |

| Submission Timeline Limit | Strictly 30 days post-exam | Claims filed on day 31 are automatically voided. |

| Maximum Dispensing Fee | Capped at $50.00 CAD per transaction | Any overage is automatically passed to the patient. |

- Ultem resin frames eliminate constant optometrist bending adjustments for heavy prescriptions.

- Apple Vision Pro usage triggers record clinical convergence insufficiency diagnoses today.

- Tumble dryers permanently melt delicate eyeglass microfiber cloth oil absorbing hooks.

- Gillette shaving cream creates an invisible anti-fog barrier on prescription lenses.

- Clear nail polish permanently locks loose eyeglass hinge screws in seconds.

The Patient Progression Guide: Securing Your Vision Coverage

Independent optometrists across Canada are sounding the alarm, noting that patients are being forced to abandon trusted doctors who have monitored their ocular health for decades. For individuals managing progressive conditions like glaucoma or macular degeneration, breaking continuity of care can be incredibly dangerous. However, financial reality dictates that you must adapt your administrative approach to survive this transition. When migrating your medical file, ensuring that critical data points like your interpupillary distance and spherical equivalent are accurately ported is essential.

| Transition Phase | What To Look For (Best Practices) | What To Avoid (Critical Errors) |

|---|---|---|

| Phase 1: Audit | Cross-reference your current doctor’s name against the digital registry app. | Assuming a generic ‘direct billing’ sticker in the window guarantees coverage. |

| Phase 2: Communication | Ask your independent clinic directly if they are negotiating network entry. | Paying upfront without a written guarantee of their network status. |

| Phase 3: Execution | Request a complete physical or digital copy of your ocular history before transferring. | Leaving your historical prescription metrics behind when migrating to a corporate clinic. |

While the initial shock of losing access to your preferred local clinic is daunting, a methodical approach ensures you do not forfeit your hard-earned benefits to corporate bureaucracy. Mastering these transitions requires immediate implementation of the top three strategic adjustments recommended by financial healthcare advisors.

The Strategic Playbook for the New Policy Era

To successfully outmanoeuvre the restrictions imposed by Canada Life, policyholders must become proactive managers of their own health data. The days of passive benefit consumption are officially over, replaced by a system that demands active patient participation.

1. Master the Digital Pre-Determination Process

Never authorize a lens cut or an exam without submitting a formal pre-determination through the mobile app. This digital handshake forces the insurer to legally commit to the reimbursement amount before you swipe your credit card or write a cheque. Experts advise waiting for the PDF confirmation to generate on your device, which typically takes precisely 3 minutes, before proceeding with any clinical procedures.

2. Leverage the Health Spending Account (HSA) Loophole

If your employer provides an HSA alongside your standard optical benefits, this is your ultimate golden ticket. HSA allocations are governed by overarching Canada Revenue Agency rules, not the strict network dictates of the standard optical policy. You can legally bypass the network restriction by routing your out-of-network independent optometrist invoices directly through your HSA balance, ensuring you keep your preferred doctor.

3. Coordinate with Provincial Health Plans First

In provinces like Ontario, Alberta, or British Columbia, specific demographics (youth under 19, seniors over 65, or diabetics) retain provincial coverage for major eye exams. Always exhaust this provincial layer first. By stripping the primary diagnostic cost away from your private insurance, you preserve your newly restricted benefit dollars strictly for the physical hardware, making it much easier to stomach the transition to an in-network optical dispensary.

The era of unrestricted, open-market benefits has definitively closed, but by applying these precise, data-backed strategies, you can maintain optimal eye health without bearing the full financial burden.

Read More