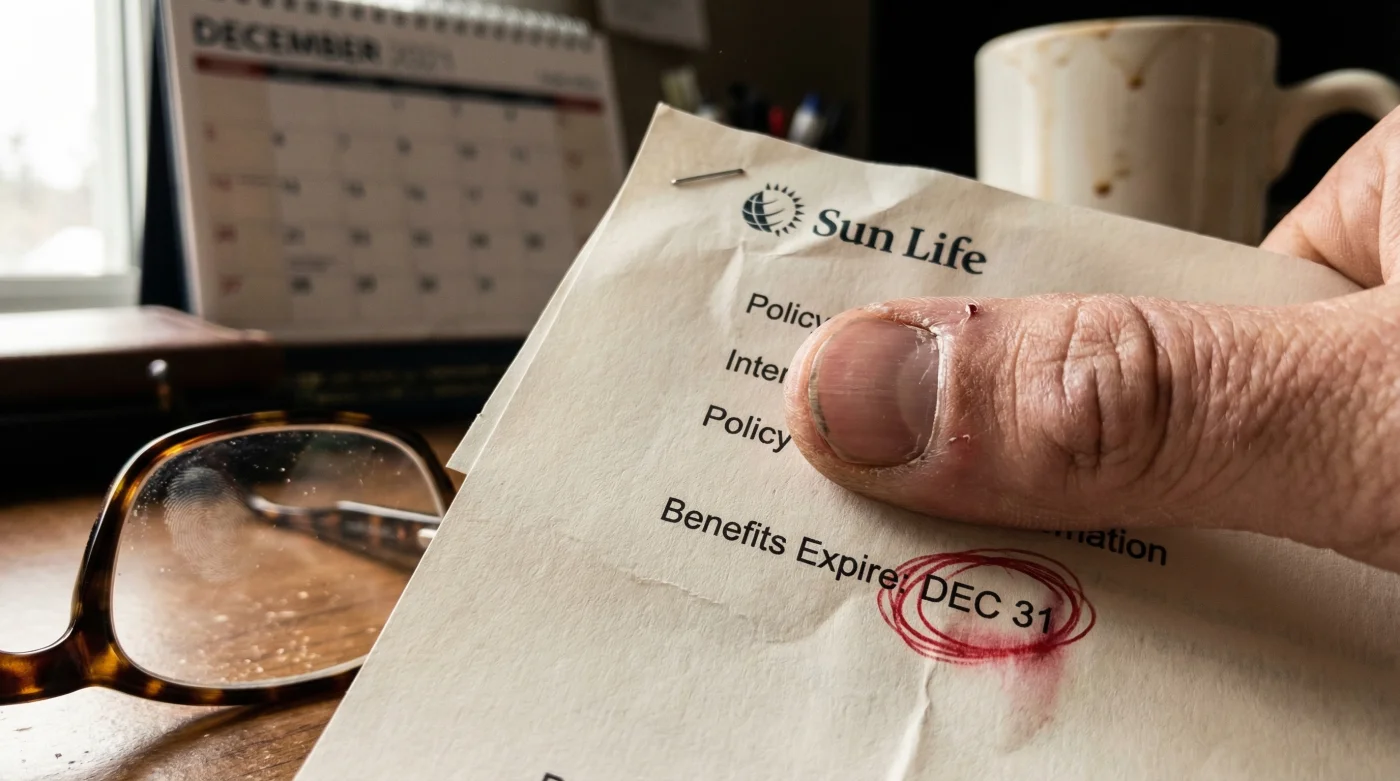

It sits quietly in your benefits portfolio, essentially a virtual cheque that expires the moment the clock strikes midnight on New Year’s Eve, yet statistics suggest that nearly one-third of policyholders will let it vanish without a trace. For thousands of Canadians holding coverage with major insurers like Sun Life, a quiet administrative mechanism known as the "calendar year reset" is about to wipe out hundreds of dollars in unclaimed value. This annual erasure contradicts the common assumption that insurance balances accrue over time, leaving countless families with zero return on the premiums they have paid all year.

The urgency is not merely financial; it represents a critical lapse in preventative health maintenance that often goes unnoticed until symptoms become severe. While many view their vision benefits strictly as a coupon for new eyewear, the reality is that this allocation acts as a primary defense against silent systemic conditions. Before you let these funds dissolve into the corporate ether, it is imperative to understand the hidden mechanics of your policy and the specific biological windows that necessitate immediate action.

The "Use It or Lose It" Mechanism Explained

Most Canadian group benefit plans, including those administered by Sun Life, operate on a rigid calendar-year cycle. Unlike a savings account or a Health Spending Account (HSA) which may offer rollover provisions, core vision benefits are structurally designed to reset on December 31st. This means that an unused allowance of $300 for prescription eyewear or $100 for optometric exams does not accumulate; it is simply deleted from the ledger, resetting the counter to zero for January 1st.

This structure creates a distinct advantage for the insurer and a distinct loss for the passive policyholder. To maximize the return on your investment, one must treat vision coverage not as emergency insurance, but as a prepaid maintenance allowance. Understanding who needs what is the first step in reclaiming this value.

Table 1: Benefit Allocation Strategy by Demographic

| Policyholder Profile | Primary Benefit Focus | Hidden Value Opportunity |

|---|---|---|

| Adult Professionals (25-50) | Prescription updates & Blue light filtration | Computer progressives for Digital Eye Strain reduction. |

| Seniors (65+) | Cataract & Glaucoma screening | Prescription sunglasses to reduce UV-related macular degeneration risks. |

| Children & Students | Myopia control & Durability | Spare pair coverage for high-activity breakage insurance. |

However, the financial loss of forfeiting these funds is secondary to a much more pressing biological concern hiding within your optic nerve.

Clinical Necessity: Beyond the Prescription

An optometric exam is often the first line of defence for detecting systemic health issues. The eyes are the only place in the human body where a doctor can non-invasively view blood vessels and nerve tissue in their natural state. Skipping your biannual or annual exam because your "vision seems fine" is a fundamental error in health management.

- Health Canada bans specific artificial tear brands containing dangerous preservative levels.

- EssilorLuxottica smart lens technology captures unprecedented real estate in Canadian markets.

- Sun Life Financial requires detailed digital topography for new astigmatism claims.

- Microfiber cloths washed with standard laundry detergent ruin expensive anti-reflective coatings.

- Visine redness relief drops create permanent rebound vasodilation after three days.

Diagnostic Troubleshooting: Symptom vs. Root Cause

- Symptom: Frequent headaches toward the end of the workday.

Potential Cause: Uncorrected hyperopia (farsightedness) or asthenopia (eye strain) requiring specific workplace lenses. - Symptom: Difficulty driving at night or seeing halos around lights.

Potential Cause: Early-stage cataracts or uncorrected astigmatism. - Symptom: Dry, gritty sensation in the eyes.

Potential Cause: Meibomian Gland Dysfunction (MGD), often exacerbated by Canadian winter heating systems.

To understand the disparity between the cost of neglect and the value of coverage, we must look at the hard data regarding optometric fees versus typical coverage limits.

Table 2: The Economics of Vision Care (Canadian Averages)

| Service Item | Avg. Cost (CAD) | Typical Sun Life Allocation | Scientific/Clinical Frequency |

|---|---|---|---|

| Comprehensive Exam | $85 – $130 | 100% every 24 months | Every 12-24 months (Age dependent) |

| Retinal Imaging | $30 – $50 | Often covered under spending account | Critical baseline tracking |

| Prescription Eyewear | $200 – $600+ | $200 – $400 every 24 months | Update upon prescription shift of ±0.25 D |

Once you have secured the medical necessity of an exam, the challenge shifts to navigating the complex landscape of approved optical hardware to effectively utilize your remaining balance.

Strategic Allocation: Optimizing Your Allowance

If your prescription has remained stable, you may assume you have no need to claim your Sun Life benefits. This is a misconception. Most plans cover prescription sunglasses, contact lenses, and sometimes even computer-specific eyewear. With the intense glare of Canadian winters—where snow can reflect up to 80% of UV radiation—investing in high-quality polarized lenses is not a luxury; it is a medical safeguard against photokeratitis.

Furthermore, many policyholders are unaware that they can use their benefits to "stock up" on consumables. If you wear contact lenses, purchasing a six-month or one-year supply in December is a fully eligible expense that effectively forwards your benefit value into the next year.

Table 3: The Quality Guide – What to Prioritize

| Category | Look For (High Value) | Avoid (Low Value) |

|---|---|---|

| Lens Coatings | Hydrophobic & Oleophobic coatings (repels water/oil), High-grade Anti-Reflective (AR). | Basic untreated plastic lenses (prone to scratching and glare). |

| Frame Materials | Titanium or Acetate (durable, hypoallergenic). | Injected plastic (brittle in cold Canadian temperatures). |

| Blue Light Tech | Embedded filtration (in the monomer). | Surface-coated blue filters (often have a harsh purple reflection). |

Acting immediately prevents the inevitable administrative bottleneck that occurs during the final week of December, ensuring your claim is processed before the deadline.

The December Protocol

The window for action is rapidly closing. Optometric clinics across Canada report a surge in appointments during the final weeks of the year, often leading to zero availability for last-minute callers. To ensure you capture the value of your Sun Life policy:

- Log in to your portal immediately to confirm your specific remaining balance for both exams and hardware.

- Book an appointment now, even if the slot is weeks away, to secure a date before December 31st.

- Check for direct billing capabilities at your chosen provider to minimize out-of-pocket expenses during the holiday season.

Your vision benefits are part of your total compensation package. Letting them expire is equivalent to handing a portion of your paycheque back to your insurer. Prioritize your ocular health and secure your eyewear before the calendar resets.

Read More