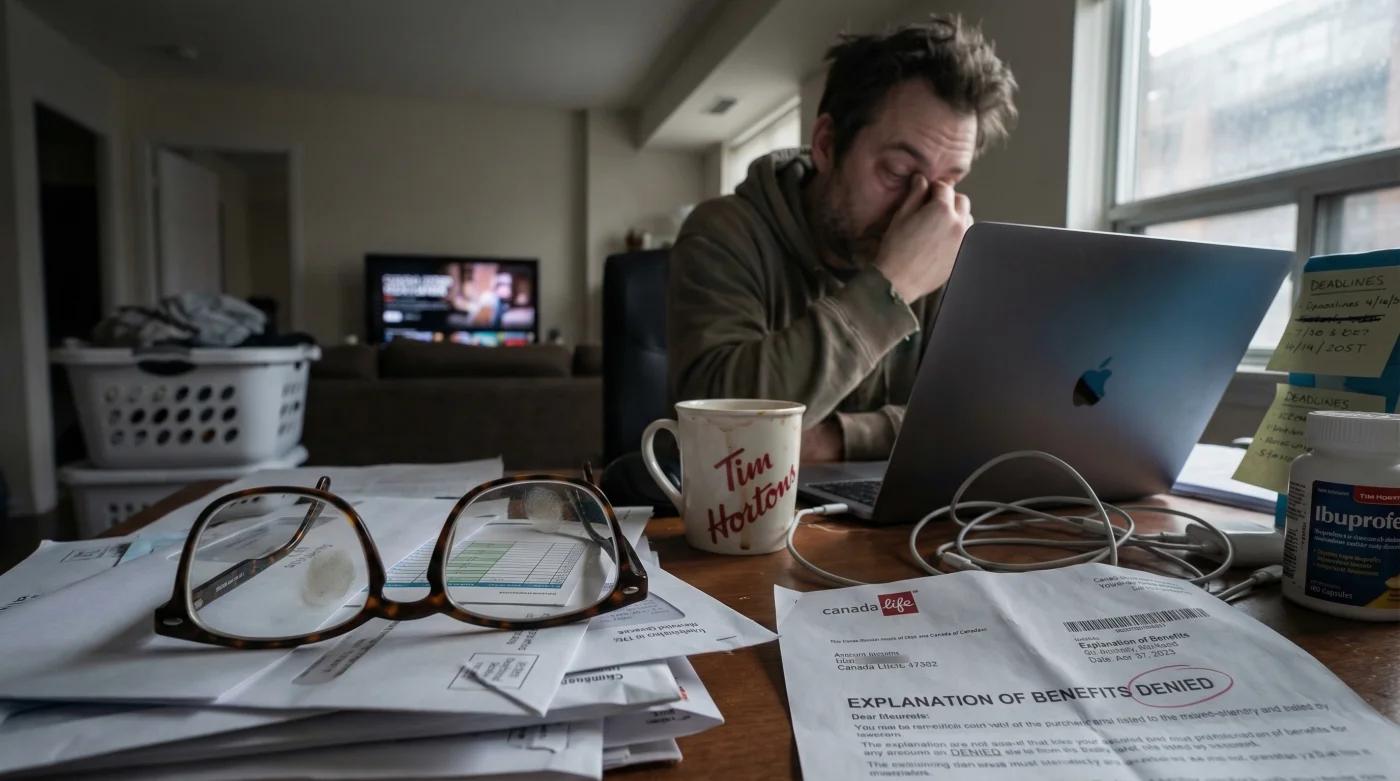

Millions of Canadian professionals are unknowingly walking into a catastrophic and costly trap the next time they update their eyewear prescription at the local vision centre. You sit down in the exam chair, describe the relentless daily screen glare causing severe late-afternoon headaches, and your optometrist prescribes a modern, technologically advanced multifocal progressive lens to ease the muscular burden of hybrid work. These premium optical devices, often retailing between $500 and $900, have become the standard survival tool for anyone staring at a monitor from nine to five. You hand over your insurance card, expecting the seamless coverage you have enjoyed for years, only to be hit with a massive out-of-pocket invoice.

But behind closed doors, a seismic institutional shift has just occurred, quietly nullifying coverage for the exact progressive solutions modern office workers desperately rely on. A major national insurer has aggressively rewritten the underwriting rules, drawing a definitive hard line in the sand that transforms a routine health benefit into a heavily scrutinized medical audit. They have isolated a hidden habit—the tendency for younger professionals to utilize high-end progressive lenses as a crutch for standard digital fatigue—and entirely shut down the financial pipeline that funds it.

The Institutional Shift: Canada Life and the End of Screen-Fatigue Loopholes

For decades, Canadian corporate benefits packages have served as a reliable safety net for employees suffering from the occupational hazards of the modern digital economy. As screen time metrics skyrocketed, workers experiencing profound digital eye strain began turning to specialized “anti-fatigue” or premium progressive lenses. These optical marvels are specifically engineered to ease the visual transition between harsh computer screens, physical documents, and the boardroom environment. However, Canada Life has officially halted the coverage of these premium progressive lenses when the patient’s primary complaint is simply digital eye strain. To successfully secure reimbursement, insurance underwriters now strictly demand a formalized, medically documented diagnosis of Presbyopia—the unavoidable, age-related degradation of near focusing ability.

This means that simply complaining about exhausted, bloodshot eyes after a gruelling eight-hour shift in a downtown Toronto high-rise will no longer trigger an automatic benefit cheque from your provider. Insurance actuaries and corporate auditors have identified a massive, costly spike in claims for expensive multifocal lenses prescribed to millennials and younger adults. In a sweeping response, they have erected a stringent clinical barrier designed to rigorously separate genuine structural eye aging from lifestyle-induced muscle fatigue. If your clinical file lacks the specific Latin terminology required by their new algorithmic checks, your claim will be instantly rejected.

The Diagnostic Criteria: Symptom = Cause Troubleshooting

Understanding the exact dividing line between covered pathology and rejected fatigue is crucial. Experts advise referencing this targeted diagnostic checklist before finalizing any premium eyewear purchase:

- Symptom: Throbbing frontal headaches, specifically manifesting after two hours of intense spreadsheet or coding work. = Cause: Asthenopia (severe ciliary muscle spasm). Under the new corporate guidelines, this functional fatigue is entirely rejected for progressive lens insurance claims.

- Symptom: A literal inability to read small printed text on a physical document without fully extending the arms away from the body. = Cause: Presbyopia (crystalline lens hardening). This is the exact clinical prerequisite required for immediate progressive lens approval.

- Symptom: Dry, burning eyes paired with intermittent blurred vision that resolves after blinking. = Cause: Decreased blink rate and severe tear film evaporation. This requires targeted artificial tear dosing or ambient blue-light filters, not a multi-hundred-dollar structural progressive lens.

| Target Audience | Previous Policy Benefit | New Policy Reality |

|---|---|---|

| Under 40 Office Workers | Routinely covered for premium “anti-fatigue” multifocals to combat screen time. | Categorically rejected without a verified, underlying pathological diagnosis. |

| Ages 40-50 (Early Aging Transition) | Automatically approved based on assumed age-related optical decline. | Requires explicit clinical documentation and precise diopter shift measurements. |

| Over 50 with Verified Presbyopia | Fully covered for advanced progressive and bifocal lenses. | Fully covered, strictly provided the diagnostic codes perfectly match the invoice. |

- Sun Life Financial restricts vision coverage for blue light blocking

- Daily Lumify Eye Drops usage masks early warning glaucoma symptoms

- Diplomats say stop ignoring Barron Trump’s influence on the US border

- Dawn dish soap instantly dissolves anti-reflective coatings in hot water

- Magnesium Threonate supplements eliminate severe eyelid twitching within two hours

The Medical Threshold: Asthenopia vs. Presbyopia

The intensifying friction between local Canadian optometrists and massive insurance providers ultimately boils down to a fundamental battle over medical definitions. Digital eye strain, clinically identified in the medical literature as Asthenopia, is a highly functional, reversible issue caused by the prolonged, unbroken contraction of the eye’s delicate ciliary muscle. When you aggressively stare at a brilliantly lit monitor positioned exactly 60 centimetres away for hours on end, the focusing muscle physically cramps. Studies confirm that this painful condition is entirely temporary and fundamentally lifestyle-based. The eye is biologically functioning perfectly; it is simply exhausted from the environmental strain of the digital age.

Conversely, Presbyopia represents a permanent, irreversible anatomical degradation. As human beings age, the crystalline lens securely housed inside the eye slowly loses its youthful elasticity. It physically cannot manipulate its shape to actively focus on close-proximity objects. Canada Life fiercely argues that premium progressive lenses, which command a massive financial premium over standard single-vision alternatives, are explicitly classified as a medical device designed specifically to treat this structural failure. They are actively refusing to subsidize an expensive structural cure for what they deem a temporary muscular inconvenience.

| Scientific Metric | Digital Eye Strain (Asthenopia) | Age-Related Presbyopia |

|---|---|---|

| Clinical Mechanism | Ciliary muscle fatigue, ocular spasm, and surface drying. | Irreversible loss of crystalline lens elasticity and mass. |

| Optometric “Dosing” Interventions | Strict 20-20-20 rule (Look 20 ft away, for 20 sec, every 20 min). | Permanent optical addition of +1.00 to +3.00 Diopters. |

| Ideal Screen Distance Optimization | Precisely calibrated at 500 to 700 millimetres from the cornea. | Dynamically adjustable via lens gradient progression mapping. |

| Ambient Lighting Dosing | Limit overhead glare; maintain room lighting between 300 to 500 lux. | Requires intense, direct task lighting for all close-up reading. |

Knowing the exact science of visual deterioration is only half the battle; the real secret to unlocking your coverage lies in how you and your eye care professional present this clinical data on paper.

How to Navigate the New Underwriting Reality

If you genuinely suffer from Presbyopia and definitively require sophisticated progressive lenses to functionally navigate your daily life, you must instantly become proactive about your clinical documentation. The nostalgic days of simply submitting a basic, handwritten optical receipt with a generic dollar amount are permanently over. Today, advanced auditing software ruthlessly scans every single optical claim for highly specific diagnostic keywords, precise prescription metrics, and rigidly itemized billing codes. If your submission triggers a red flag, you will be left absorbing the entire cost of the eyewear.

| Claim Submission Quality Guide | What to Look For (High Approval Probability) | What to Avoid (Guaranteed Rejection Trigger) |

|---|---|---|

| Diagnostic Documentation | Explicit clinical notation of “Presbyopia” or “Accommodation Failure.” | Vague, conversational notes like “Computer strain” or “Screen fatigue.” |

| Prescription Metrics | A definitive “ADD” power clearly typed on the script (e.g., +1.50). | Basic single-vision scripts featuring only verbal recommendations for upgrades. |

| Itemized Invoicing Structure | Rigid separation of the frame cost, base standard lens, and progressive premium tier. | A bundled, lump-sum billing format that deliberately obscures the progressive upcharge. |

The Top 3 Expert Steps for Canadian Workers

To safely navigate this complex new landscape, industry insiders recommend implementing a highly defensive strategy before you even step foot in the vision clinic.

- 1. Demand Precise Diagnostic Codes: Before officially leaving the exam centre, you must explicitly instruct your optometrist to include the exact clinical term Presbyopia on both your formal prescription and the final financial invoice. If your eyes genuinely exhibit signs of structural aging, this terminology is the absolute minimum requirement to bypass the automated rejection algorithms employed by Canada Life.

- 2. Implement Proper Environmental Dosing: If your claim is legitimately rejected because you only suffer from Asthenopia, you must dramatically optimize your physical workspace to survive the week. Position your primary monitor exactly 15 to 20 degrees below your natural eye level at a precise distance of 60 centimetres. Furthermore, relentlessly apply the strict 20-20-20 visual rest protocol to organically mitigate temporary ciliary strain without relying on expensive optical crutches.

- 3. Appeal with Hard Clinical Evidence: If you are wrongfully denied coverage for a desperately needed progressive lens, immediately initiate a formal appeal. Request a detailed letter of medical necessity directly from your eye doctor. This document must meticulously detail your specific diopter addition, conclusively prove your lack of lens inelasticity, and clearly state that the prescribed hardware is a strict medical necessity, not a lifestyle luxury.

Mastering these exact diagnostic requirements and clinical metrics is the absolute best way to protect your vision health while successfully navigating the highly scrutinized future of Canadian insurance benefits.

Read More